Municipals were weaker Thursday as outflows from muni mutual funds returned and U.S. Treasuries saw yields rise out long. Equities sold off.

Triple-A benchmarks were cut three to nine basis points, depending on the scale, while UST yields rose up to four basis points out long, pushing the 10- and 30-year to multi-year highs.

The two-year muni-to-Treasury ratio Thursday was at 63%, the three-year at 64%, the five-year at 64%, the 10-year at 66% and the 30-year at 87%, according to Refinitiv MMD’s 3 p.m. read. ICE Data Services had the two-year at 63%, the three-year at 64%, the five-year at 63%, the 10-year at 65% and the 30-year at 87% at 4 p.m.

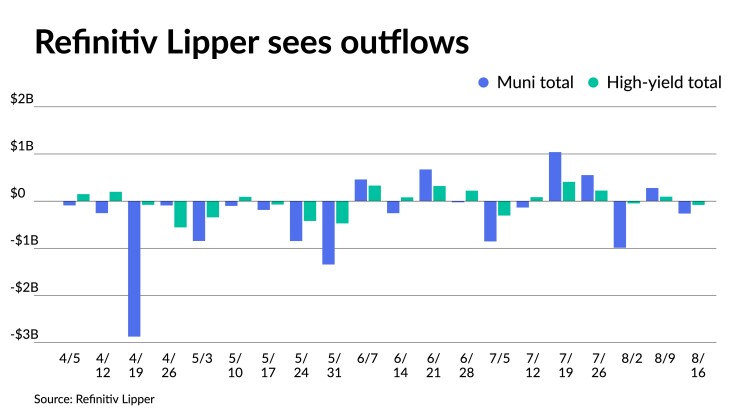

Refinitiv Lipper reported $264.046 million of outflows from municipal bond mutual funds for the week ending Wednesday after $278.449 million of inflows into the funds the previous week.

“Positive early August momentum has been offset by late-summer vacations and a jump higher in UST rates,” said James Pruskowski, chief investment officer at 16Rock Asset Management.

While supply and reinvestment conditions are still favorable, he said “tight UST ratios are causing munis to have a larger reaction function.”

UST rates are “testing support as issues around longer-term growth, term premium, and issuance remain top of mind,” he said.

Mid-month momentum “has been stymied by late-summer vacation schedules and a UST market that has been in a one-way trade up in yield for five straight sessions,” said Kim Olsan, senior vice president of municipal bond trading at FHN Financial.

“The angst for munis is that reinvestment totals and supply conditions are still constructive but fading ratios could mean that generic yields begin to adjust accordingly,” she said.

Following cuts out long on Refinitiv MMD’s scale Thursday, the 10-year flew past its high of 2.77% from early August to land at 2.84%, while the 10-year UST trades reached a 15-year high at 4.29%.

Since 2018, she noted “the 10-year MMD spot has traded as narrowly as six basis points (2018) to as wide as 45 basis points (2022), but August 2019 did produce a 27 basis point range.”

The month has seen an average loss of 1% in the last three years, she said.

“This year there is the overhang of FOMC actions, as there was last year; however, the approaching end or neutrality of the tightening cycle should mean munis sustain a higher yield through the end of Q4 than has occurred dating back to 2011,” Olsan said. Over a broader horizon since 2000, she said the 10-year MMD average yield is 2.80%, which is a five basis point difference from Wednesday.

“What may begin to develop is a bilateral market, whereby general market names widen out further than the handful of states … that can’t supply enough bonds for existing inquiry,” she said.

A full new-issue calendar, which included two state GO sales, “shed light on buyers’ perspectives as to fair value,” according to Olsan.

Tennessee sold state GOs “at interesting concessions due to an extraordinary redemption provision tied to a new stadium project completion,” she said.

The 10-year maturity was “spread +29/MMD, or about 20 basis points above that of noncallable Tennessee GOs,” she said.

Other issuance, including airport deals, “reflected the widening gap in AMT-subject paper,” she said.

Atlanta’s non-AMT series “offered a 10-year at 3.13% with the AMT series spread 52 basis points wider. In the 20-year maturity, the AMT yield variance amounted to 32 basis points vs. the non-AMT bond,” she said.

Meanwhile, the cities of Dallas and Fort Worth, Texas, “10-year non-AMT yield was 3.41% and the AMT series yielded 3.92%, a comparable gap to the Atlanta pricing,” she said.

A 2042 DFW non-AMT maturity “offered a yield of 4.05%, spread +61/MMD,” according to Olsan.

Issuance for AMT deals is down 42% year-over-year at $8 billion in volume, according to Bloomberg.

“Interpolating supply for the full year would place the total at under $10 billion, or comparable to 2020’s total but well off the $21 billion issued in 2019 and 2022,” she said.

In the primary market Thursday, BofA Securities priced for the Los Angeles Unified School District (A2//A-/) $381.100 million of sustainability certificates of participation, 2023 Series A, with 5s of 10/2024 at 3.34%, 5s of 2028 at 3.10%, 5s of 2033 at 3.25% and 5s of 2038 at 3.76%, callable 10/1/2033.

Goldman Sachs priced for the Dormitory of the State of New York (Aa2//AA/) $293.670 million of The New York and Presbyterian Hospital Obligated Group revenue bonds, with 5s of 8/2029 at 3.01%, 5s of 2033 at 3.16% and 5s of 2038 at 3.67%, callable 8/1/2033.

Secondary trading

North Carolina 5s of 2024 at 3,28%. NYC 5s of 2024 at 3.16%-3.05% versus 3.22%-3.17% Wednesday and 3.25% Tuesday. Massachusetts 5s of 2024 at 3.22% versus 3.22%-3.20% Wednesday.

Ohio 5s of 2028 at 2.98%. NYC TFA 5s of 2028 at 2.84%-2.85%. California 5s of 2029 at 2.78%.

NYC 5s of 2032 at 3.03% versus 2.99%-3.01% Tuesday and 2.97% on 8/11. DASNY 5s of 2035 at 3.23%-3.22% versus 3.23% on 8/4 and 3.23% original on 8/3. Virginia College Building Authority 5s of 2036 at 3.22%.

Huntsville, Alabama, 5s of 2046 at 4.02%-3.89%. NYC 5s of 2051 at 4.19%-4.32% versus 4.19%-4.04% Wednesday and 4.22%-4.20% Tuesday.

AAA scales

Refinitiv MMD’s scale was cut five to nine basis points: The one-year was at 3.25% (+5) and 3.15% (+5) in two years. The five-year was at 2.84% (+7), the 10-year at 2.84% (+9) and the 30-year at 3.82% (+9) at 3 p.m.

The ICE AAA yield curve was cut three to eight basis points: 3.24% (+4) in 2024 and 3.16% (+3) in 2025. The five-year was at 2.83% (+5), the 10-year was at 2.79% (+7) and the 30-year was at 3.81% (+8) at 4 p.m.

The S&P Global Market Intelligence (formerly IHS Markit) municipal curve was cut out long: 3.26% (+5) in 2024 and 3.15% (+5) in 2025. The five-year was at 2.85% (+7), the 10-year was at 2.85% (+9) and the 30-year yield was at 3.81% (+9), according to a 4 p.m. read.

Bloomberg BVAL was cut up five to seven basis points: 3.24% (+5) in 2024 and 3.14% (+5) in 2025. The five-year at 2.82% (+5), the 10-year at 2.80% (+7) and the 30-year at 3.80% (+7) at 4 p.m.

Treasuries were weaker out long.

The two-year UST was yielding 4.942% (-4), the three-year was at 4.668% (-1), the five-year at 4.424% (+1), the 10-year at 4.293% (+3), the 20-year at 4.584% (+4) and the 30-year Treasury was yielding 4.400% (+4) at the close.

Mutual fund details

Refinitiv Lipper reported $264.046 million of outflows from municipal bond mutual funds for the week ending Wednesday following $278.449 million of inflows the week prior.

Exchange-traded muni funds reported outflows of $63.203 million versus $281.644 million of inflows in the previous week. Ex-ETFs muni funds saw outflows of $200.843 million after $3.195 million outflows in the prior week.

Long-term muni bond funds had $53.095 million of inflows in the latest week after inflows of $444.929 million in the previous week. Intermediate-term funds had $18.771 million of outflows after $80.979 million of inflows in the prior week.

National funds had outflows of $245.765 million versus $303.621 million of inflows the previous week while high-yield muni funds reported outflows of $81.993 million versus inflows of $93.945 million the week prior.

July FOMC minutes

The key takeaway from the July Federal Open Market Committee meeting minutes “is that although policymakers remain concerned by upside inflation risks, tentative signs of easing inflationary pressures and incremental loosening in labor markets has somewhat softened the Fed’s inflation-fighting zeal,” said Mickey Levy, chief economist for Americas and Asia at Berenberg Capital Markets and a member of the Shadow Open Market Committee.

“The minutes showed a Committee split on how much more policy tightening is needed,” Morgan Stanley strategists said.

They noted that the September FOMC meeting “remains a live decision that will depend on the totality of the data, a view likely to be stressed by Chair Powell at Jackson Hole next week.”

“We continue to see a path to no further hikes,” they added.

Levy, though, said that “to retain optionality, policymakers are likely to stress that further rate hikes will remain on the table through year-end, although our expectation is that economic data over the latter half of this year will the keep the Fed on hold.”

Edward Moya, senior market analyst at OANDA, concurred with Levy, saying the minutes “will show that policymakers are not convinced their rate-hiking campaign is over.”

Officials, he noted, “will likely remain optimistic that the US economy may avoid a recession, but still are unsure over the impact of deteriorating credit conditions.”

The details of the minutes “suggest that while the ultimate decision to raise rates was unanimous, two participants at the June FOMC meeting would have supported keeping rates unchanged, with some participants continuing to flag downside risks to activity and upside risks to unemployment, while ‘a number of participants’ stressed that risks had ‘become more two-sided’ and that it would be important to balance the risks around under- and over-tightening,” Levy said.

This slight dovish shift appears “to have been underpinned by a broad-based recognition by policymakers that the stance of policy is now ‘restrictive’ and weighing on economic activity, inflation, and labor markets,” he said.

Powell “unequivocally underscored this view at the July post-meeting press conference, emphasizing that the Fed had raised rates by 525 basis points since March 2022 and that monetary policy is ‘restrictive and … putting downward pressure on economic activity and inflation,'” he added.

Given recent subdued inflation readings, he expects “Fed members to make downward revisions to their estimates of PCE inflation when they publish their quarterly economic and policy rate forecasts at the September FOMC meeting.”

However, Levy said “Fed members will likely continue to reiterate that risks to inflation remain tilted to the upside, with the July minutes suggesting policymakers view more resilient than expected economic activity as potentially exacerbating inflationary pressures over the medium term.”

He noted that “Fed members remain uncertain over the cumulative, lagged effects of monetary policy, and are clearly engaged in a debate over how much of the Fed’s policy tightening has already transmitted to the economy.”