Municipal bonds were weaker Tuesday as U.S. Treasury yields rose out long and equities sold off.

The two-year muni-to-Treasury ratio Tuesday was at 69%, the three-year was at 70%, the five-year at 71%, the 10-year at 73% and the 30-year at 90%, according to Refinitiv Municipal Market Data’s 3 p.m., ET, read. ICE Data Services had the two-year at 69%, the three-year at 71%, the five-year at 70%, the 10-year at 72% and the 30-year at 91% at 3 p.m.

“The reality of ‘higher for longer’ is settling in not only on investors’ psyche but also on their behavior too,” said Tom Kozlik, managing director and head of public policy and municipal strategy at HilltopSecurities.

Yields have “risen substantially over the last week as the market seeks to find at least a minor level of balance or equilibrium,” he said.

Muni yields were weaker Tuesday, as triple-A benchmarks were cut three to five basis points, depending on the scale.

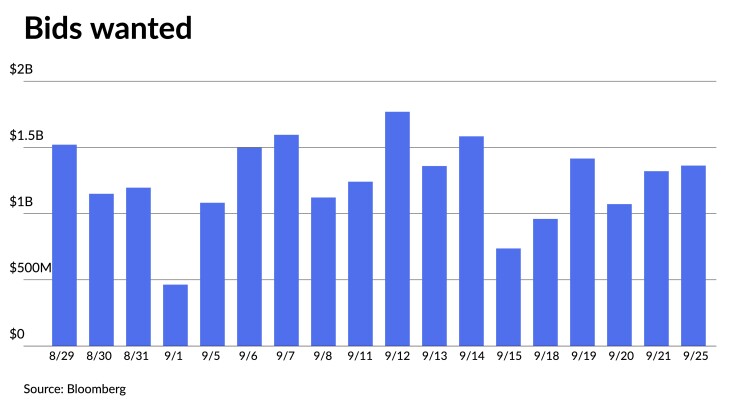

This continues the sell-off from last week, where tax-exempt yields corrected more than 20 basis points across the curve, said Matt Fabian, a partner at Municipal Market Analytics.

“Municipal losses [last week] came on lower trade volumes, or at least lower than the week before, meaning this was more about price correction, in particular via offered-side scales and reasonable dealer caution in setting primary market prices,” Fabian said.

Fund outflows the week before — the seventh consecutive ——when “combined with low reinvestment, heavier trading volumes (by par), and an accelerating bank pullback from municipals had created a context for weakness,” he said.

“Then the Fed, which, although not raising rates again, suggested higher-for-longer, which will have further discouraged any accounts waiting for slower economic data to signal a Fed pivot and thus a potential bond rally,” Fabian noted. “A bond rally seems unlikely in 2023.”

Additionally, more fund outflows and fund NAV losses “will complicate marketing efforts just when seasonal reinvestment flows are about to begin typical autumn diets,” he said.

These vectors are “gutting institutional demand and compelled dealers to bring even a smaller-sized primary calendar at deep concessions to the secondary, allowing block trades of key new issues (Philly water and Massachusetts GOs) to break to stronger prices (after adjusting for AAA benchmark movements),” he said.

So “while the market as a whole would appear to lack much near-term bounce potential absent an unexpected and sustained surge in UST prices, it is presenting excellent opportunities for buyers able to manage unpredictable volatility and maybe unflattering total return into year end,” he said.

Yields, for example, continue to be attractive, Kozlik said. Prior to the Fed meeting, munis yields were appealing, but they are even more so today, he noted.

However, he said, attractive yields are not “being gobbled up largely because market supply is outpacing narrow demand at the moment.

Overall, he has a positive view of the municipal sector given “how strong credit quality is even in the face of uncertainty, such as a potential government shutdown, labor uncertainty, and rising oil prices.”

He believes “state and local government credit quality is more prepared for a potential economic downturn than it has ever been.”

In the primary market Tuesday, Raymond James & Associates held a one-day retail order for $641.485 million of water and sewer system second general resolution revenue bonds, Fiscal 2024 Series AA from the New York City Municipal Water Finance Authority (Aa1/AA+/AA+/). The first tranche, $262.145 million of Series AA-1, saw 5.25s of 6/2053 at 4.65% and 5s of 2053 at 4.70%, callable 12/15/2033.

The second tranche, $164.380 million of Series AA-2, saw 5s of 6/2030 at 3.46%, callable 12/15/2028, and 5s of 2035 at 3.69%, callable 12/15/2033.

The third tranche, $214.960 million of Series AA-3, saw 5s of 6/2034 at 3.58%, make whole call; 5s of 2043 at 4.46%, callable 12/15/2033; and 5.25s of 2048 at 4.58%, callable 12/15/2033.

J.P. Morgan priced for the Missouri Health and Educational Facilities Authority (A1/A+//) $297.955 million of Mercy Health Facilities revenue bonds, with 5s of 12/2040 at 4.68%, 5.5s of 12/2043 at 4.86%, 5.5s of 2048 at 5.03% and 5s of 2052 at 5.15%, callable 12/1/2033.

Secondary market

Minnesota 5s of 2024 at 3.65%. NYC 5s of 2024 at 3.67% versus 3.55% Friday. Connecticut 5s of 2025 at 3.80% versus 3.26% on 9/8 and 3.29% on 9/6.

Georgia 4s of 2028 at 3.33%-3.32%. Maryland 5s of 2028 at 3.28%. Wisconsin 5s of 2029 at 3.37%-3.35%.

Maryland 5s of 2031 at 3.40%-3.38%. Metropolitan Atlanta Rapid Transit Authority 5s of 2032 at 3.41%-3.40%. Santa Clara Valley Transportation Authority 5s of 2036 at 3.38%-3.39%.

Triborough Bridge and Tunnel Authority 5s of 2047 at 4.55%-4.54%. Massachusetts 5s of 2048 at 4.54% versus 4.35%-4.34% Thursday and 4.16%-4.15% on 9/12. San Jose Financing Authority 5s of 2052 at 4.24%-4.21%.

AAA scales

Refinitiv MMD’s scale was cut up five basis points: The one-year was at 3.62% (+5) and 3.54% (+5) in two years. The five-year was at 3.27% (+5), the 10-year at 3.31% (+5) and the 30-year at 4.22% (+5) at 3 p.m.

The ICE AAA yield curve was cut three to four basis points: 3.61% (+3) in 2024 and 3.55% (+3) in 2025. The five-year was at 3.26% (+3), the 10-year was at 3.28% (+3) and the 30-year was at 4.24% (+3) at 4 p.m.

The S&P Global Market Intelligence (formerly IHS Markit) municipal curve was cut up three to five basis points: The one-year was at 3.63% (+5) in 2024 and 3.54% (+5) in 2025. The five-year was at 3.29% (+5), the 10-year was at 3.31% (+5) and the 30-year yield was at 4.20% (+3), according to a 3 p.m. read.

Bloomberg BVAL was cut four to five basis points: 3.60% (+5) in 2024 and 3.52% (+5) in 2025. The five-year at 3.24% (+5), the 10-year at 3.31% (+5) and the 30-year at 4.27% (+5) at 4 p.m.

Treasuries were weaker out long.

The two-year UST was yielding 5.126% (+1), the three-year was at 4.832% (+1), the five-year at 4.615% (flat), the 10-year at 4.551% (+1), the 20-year at 4.689% (+3) and the 30-year Treasury was yielding 4.689% (+3).

Primary to come

The Texas Water Development Board (/AAA/AAA/) is set to price Wednesday $1.003 billion of state water implementation revenue fund bonds, consisting of $998.125 million of tax-exempts, Series 2023A, serials 2024-2038, terms 2039, 2040, 2041, 2042, 2043, 2044, 2046, 2048, 2051, 2053 and 2058, and $5.095 million of taxable, Series 2023B, serials 2024-2038, terms 2043 and 2053. Wells Fargo Bank.

The California State Public Works Board (Aa3/A+/AA-/) is set to price Wednesday $625.235 million of various capital projects lease revenue refunding bonds, 2023 Series C. Goldman Sachs.

New York State is set to price Thursday $542.865 of GOs, consisting of $213.135 million of tax-exempts, Series 2023A, serials 2025-2041; $236.135 of tax-exempts, Series 2023B, serials 2025-2041; $83.435 million of tax-exempt refunding bonds, Series 2023C, serials 2024-2042; and $10.160 million of taxables, Series 2023D, serial 2024. BofA Securities.

The Wayne County Airport Authority (A1//A/AA-/) is set to price Wednesday $375.025 million of airport revenue bonds on behalf of the Detroit Metropolitan Wayne County Airport, consisting of $108.360 million of Series A, serials 2026-2043, terms 2048; $82.470 million of Series B, serials 2026-2043, term 2048; $137.760 million of Series C, serials 2024-2042; $18.225 million of Series D, serials 2024-2037; and $28.210 million of Series E, serial 2028. Siebert Williams Shank & Co.

The Pennsylvania Economic Development Financing Authority (/A-//) is set to price Wednesday $150 million of solid waste disposal revenue bonds, Series 2021A-2, serial 2046. BofA Securities.

Durham, North Carolina, (Aa1/AA+/AA+/) is set to price Thursday $128.300 million of limited obligation bonds, Series 2023, serials 2024-2043. PNC Capital Markets.

The San Francisco Public Utilities Commission (/AA/AA-/) is set to price Wednesday $121.660 million of power revenue bonds, 2023 Series A. J.P. Morgan Securities.

Competitive

Rutherford County, Tennessee, (Aaa/AA+//) is set to sell $175 million of GOs at 10:30 a.m eastern Wednesday.