Municipals were mixed Thursday in secondary trading as focus shifted to California’s nearly $1.5 billion of tax-exempt and taxable general obligation bond deals in the competitive market while U.S. Treasuries were weaker out long after Wednesday’s short-end selloff and equities were in the black at the close.

Triple-A yield curves saw a mix of bumps and cuts while Treasuries saw small gains on the short end and losses outside of five years.

Muni-to-UST ratios were little moved on the day’s session. The two-year muni-to-Treasury ratio Thursday was at 64%, the three-year at 62%, the five-year at 60%, the 10-year at 60% and the 30-year at 83%, according to Refinitiv Municipal Market Data’s 3 p.m. EST read. ICE Data Services had the two-year at 63%, the three-year at 62%, the five-year at 60%, the 10-year at 61% and the 30-year at 83% at 3:30 p.m.

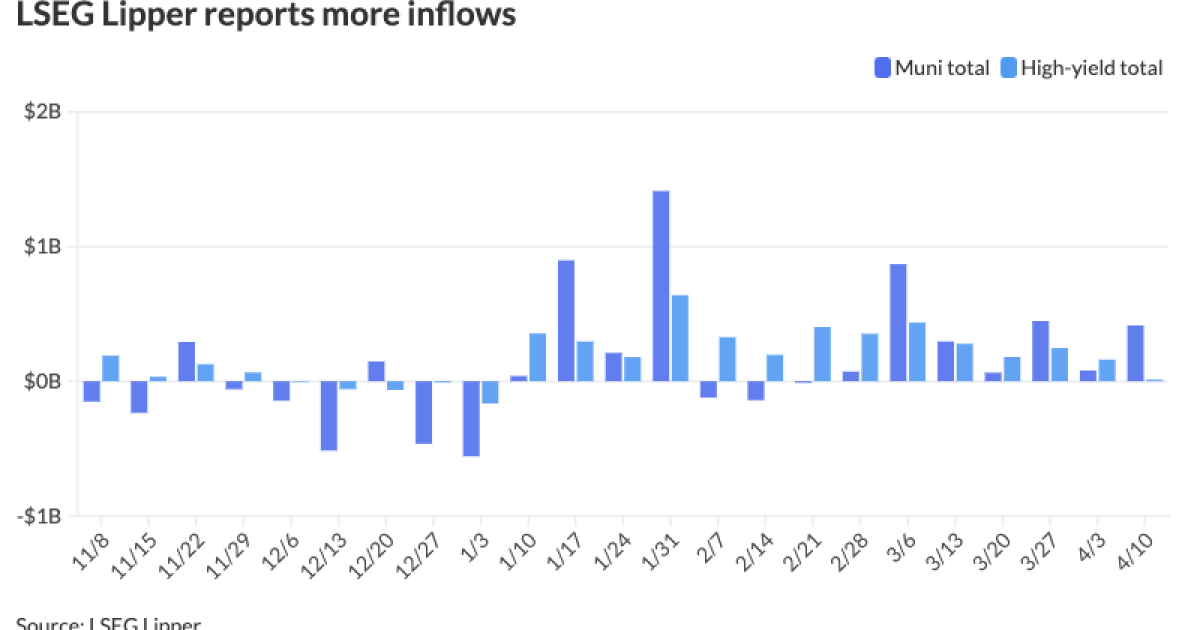

Municipal bond mutual funds posted another week of inflows, the seventh consecutive week in positive territory for the fund complex and the 14th week of inflows for high-yield funds.

LSEG Lipper reported fund inflows of $414.5 million for the week ending Wednesday following $79.9 million of inflows the prior week.

High-yield muni bond funds saw another round of inflows, but much smaller, at $11 million compared to last week’s inflows of $161.1 million.

In the competitive market Thursday, California (Aa2/AA-/AA/) sold $600 million of tax-exempt various purpose GOs, Bid Group C, to BofA Securities, with 4s of 9/2025 at 3.21%, 4s of 2028 at 2.85%, 5s of 2034 at 2.85%, 5s of 2039 at 3.25%, 5s of 2044 at 3.64%, 4s of 2047 at 4.05% and 4s of 2052 at 4.135%, callable 3/1/2034.

The state also sold $442.835 million of taxable various purpose GOs, Bid Group A, to Morgan Stanley, with 5.5s of 9/2026 at 5.09% and 5.15s of 2034 at 5.07%, noncall.

Additionally, California sold $442.390 million of taxable various purpose GOs, Bid Group B, to Barclays, with 5.125s of 9/2029 at 4.95%, noncall.

Broome County, New York, sold $113.342 million to BofA Securities, with 4.5s of 4/2025 at 3.68%, noncall.

In the negotiated market, BofA Securities priced for the Marion County School Board, Florida, (/AA//) $295.665 million of Assured Guaranty-insured certificates of participation, Series 2024, with 5s of 6/2026 at 3.30%, 5s of 2029 at 2.95%, 5s of 2034 at 3.09%, 5s of 2039 at 3.58% and 5.25s of 2044 at 3.98%, callable 6/1/2034.

“An overarching trend at the start of this year has been relatively strong valuations due to a strong technical backdrop,” said David Grean, vice president, trader and strategist at Payden & Rygel.

Demand has remained “robust” as investors continue to see value in “locking in current yield levels,” he said.

While

Due to this, new issues are “well oversubscribed,” said Ted Ruddock, managing director of Fixed Income Private Wealth at Raymond James, and Drew O’Neil, director of Fixed Income Strategy at Raymond James.

“With the tail end of the baby boomers continuing to push into retirement at the rate of over 10,000/day — nearly 4 million expected this year — there’s plenty of pent-up demand for reliable, tax-efficient income,” they said.

“Tax-exempt issuance probably continues at a pace similar to recent years as there doesn’t appear to be any real catalyst for increased supply unless [tax-exempt] advanced refundings are brought back,” Congdon said.

With the first quarter seeing a surge in supply,

BofA and CreditSights both raised their initial predictions of $400 billion to $460 billion and $450 billion, respectively.

However, those revisions could be “too aggressive for a national election year with the 10-year Treasury still well anchored in the 4.00%+ range,” Ruddock and O’Neil said.

Due to the “strong” start of the year, they believe issuance will skew toward the higher end of their initial estimate of $350 billion to $400 billion, averaging around $33 billion monthly.

In the second quarter, Ruddock and O’Neil see issuance continuing at its “robust pace.”

Ruddock and O’Neil think issuance will pick up when it usually does. For instance, they noted June historically ranks first or second for the most monthly issuance.

The effect of yields “likely depends at least as much on the economy and the Fed as it does supply-demand dynamics in the muni market,” according to Ruddock and O’Neil.

There are two Fed meetings this quarter, “when they will once again update the summary of economic projections,” they said.

The futures market is “pricing in no change for the upcoming meeting, and it’s basically a coin toss for June,” they said.

AAA scales

Refinitiv MMD’s scale was cut three basis points five years and in: The one-year was at 3.38% (+3) and 3.15% (+3) in two years. The five-year was at 2.75% (+3), the 10-year at 2.72% (unch) and the 30-year at 3.86% (unch) at 3 p.m.

The ICE AAA yield curve was bumped up to five basis points: 3.35% (-5) in 2025 and 3.14% (-4) in 2026. The five-year was at 2.77% (+1), the 10-year was at 2.76% (-1) and the 30-year was at 3.84% (unch) at 3:30 p.m.

The S&P Global Market Intelligence municipal curve was cut up to three basis points: The one-year was at 3.46% (+3) in 2025 and 3.20% (+3) in 2026. The five-year was at 2.79% (+3), the 10-year was at 2.75% (+3) and the 30-year yield was at 3.85% (unch), according to a 3 p.m. read.

Bloomberg BVAL was cut two basis points: 3.40% (+2) in 2025 and 3.18% (+2) in 2026. The five-year at 2.70% (+2), the 10-year at 2.70% (+2) and the 30-year at 3.88% (+2) at 3:30 p.m.

Treasuries were slightly weaker out long.

The two-year UST was yielding 4.939% (-3), the three-year was at 4.778% (-2), the five-year at 4.609% (flat), the 10-year at 4.567% (+2), the 20-year at 4.778% (+3) and the 30-year at 4.654% (+2) at 3:45 p.m.

FOMC minutes

Minutes of the latest Federal Open Market Committee meeting were

“The March FOMC minutes reinforce that Fed officials have been acutely focused — and uneasy — about near-term developments on the inflation front, even as they generally expect bumpy disinflation to continue,” according to BNP Paribas economists.

Although nearly the entire FOMC agreed rate cuts would be needed this year, they “lacked sufficient ‘confidence’ to initiate rate cuts given the recent data backdrop,” BNP said.

And hotter-than-expected inflation supports those officials “who cautioned that recent increases should not be discounted ‘merely as statistical aberrations,'” BNP said.

CPI validates the FOMC’s “concerns over the persistence of high inflation,” said BMO Senior Economist Jay Hawkins. “With inflation clearly heading in the wrong direction, the Fed might need to remain on hold for longer.”

Even before Wednesday’s inflation report, he quoted the minutes, which said, “participants generally noted their uncertainty about the persistence of high inflation and expressed the view that recent data had not increased their confidence that inflation was moving sustainably down to 2%.”

The minutes noted risks to the inflation outlook remain ”tilted slightly to the upside”, while economic outlook risks were “skewed a little to the downside, as any substantial setback in reducing inflation might lead to a tightening of financial conditions that would slow the pace of economic activity by more than the staff anticipated in their baseline forecast”.

Daniel Siluk, portfolio manager at Janus Henderson Investors, also noted the desire to ease policy this year after the members’ confidence level that inflation will hit their 2% target increases. As a result of inflation data, he said, “Unfortunately, the confidence they sought in inflation trends was not bolstered today.”

As a result, Siluk said, the markets are more cautious about rate cut projections. ”Expectations for the timing of the initial rate cut have shifted, with market consensus now leaning towards September.”

Gary Siegel contributed to this story.